A US/Israeli military escalation involving Iran would add significant uncertainty to global energy markets, mainly via a higher risk premium for oil and LNG. While the scale and duration of any conflict are highly uncertain, we assess the potential impact on Japan using fuel price sensitivity scenarios (special thanks to Zaheer Ahamed ), applying 10%, 20% and 40% uplifts to existing JKM gas price assumptions across the full five-year forecast horizon.

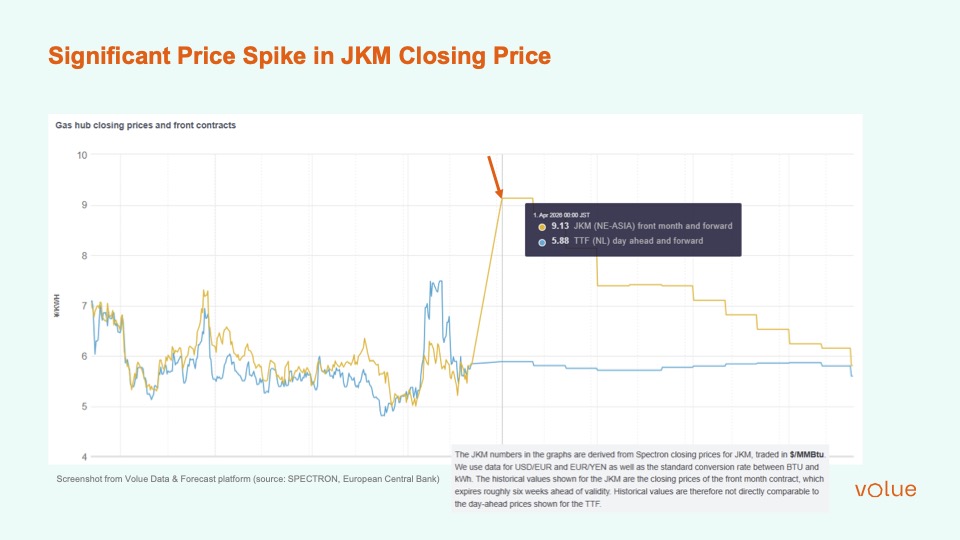

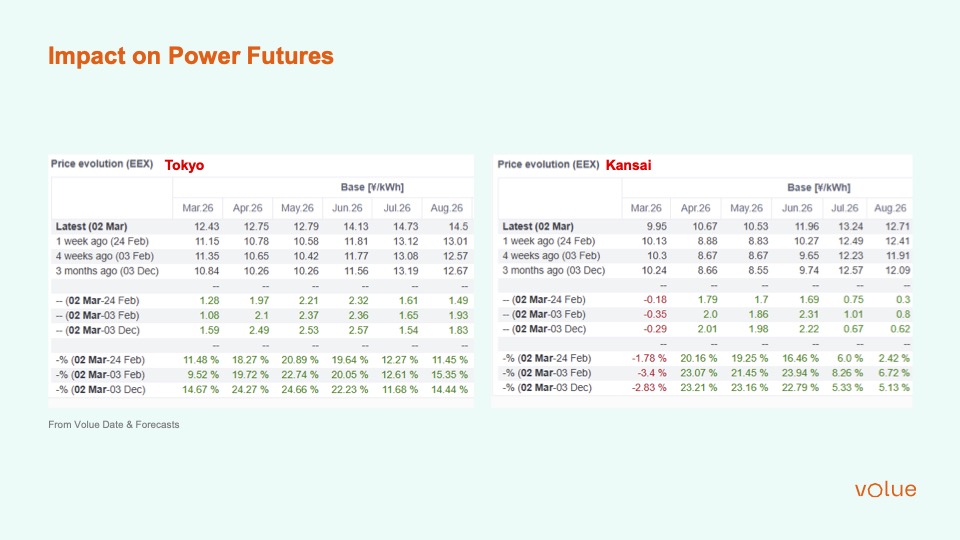

Japan is particularly exposed due to its heavy reliance on imported fossil fuels, much of which transits key Middle East shipping routes. Any sustained disruption, or higher insurance and freight costs, would therefore feed quickly into delivered fuel prices. This risk has already begun to materialise, with JKM prices rising sharply in recent days, reflecting heightened market sensitivity to Middle East developments. A similar response is visible in forward power markets, where EEX Tokyo and Kansai monthly contracts have moved materially higher.

These market moves are broadly consistent with the lower end of our +10% to +20% JKM scenarios, suggesting that part of the geopolitical risk premium is already priced into Japanese power forwards.

Japan’s LNG procurement structure further amplifies the impact. Around 70% of LNG imports are supplied under long-term contracts indexed to crude oil prices, meaning higher oil prices would raise LNG costs well beyond the spot JKM market. As a result, an oil-led geopolitical shock risks embedding higher gas costs more persistently into the power price outlook.

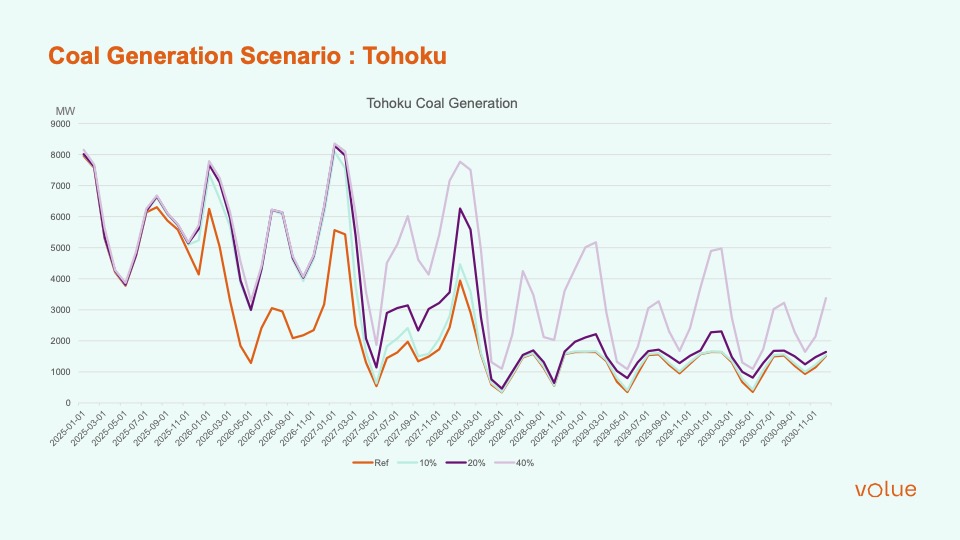

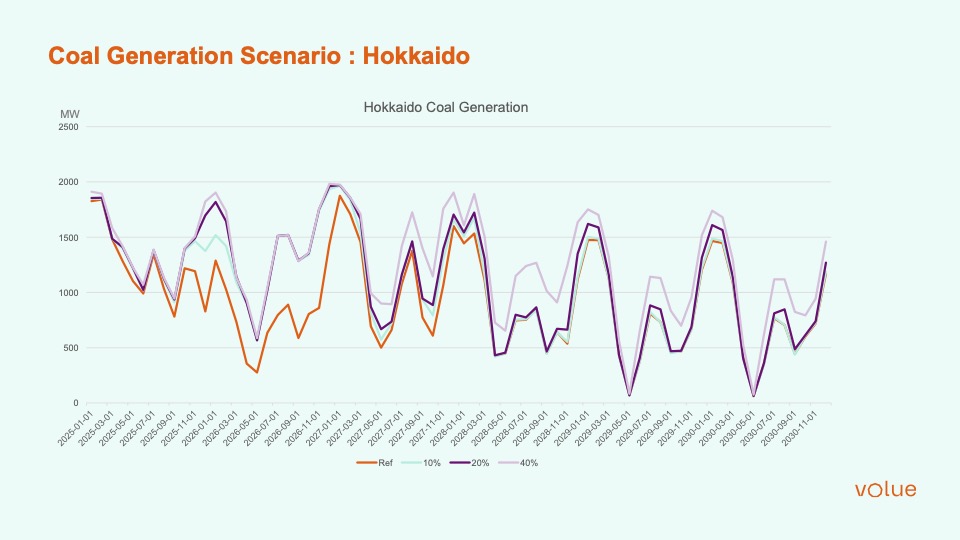

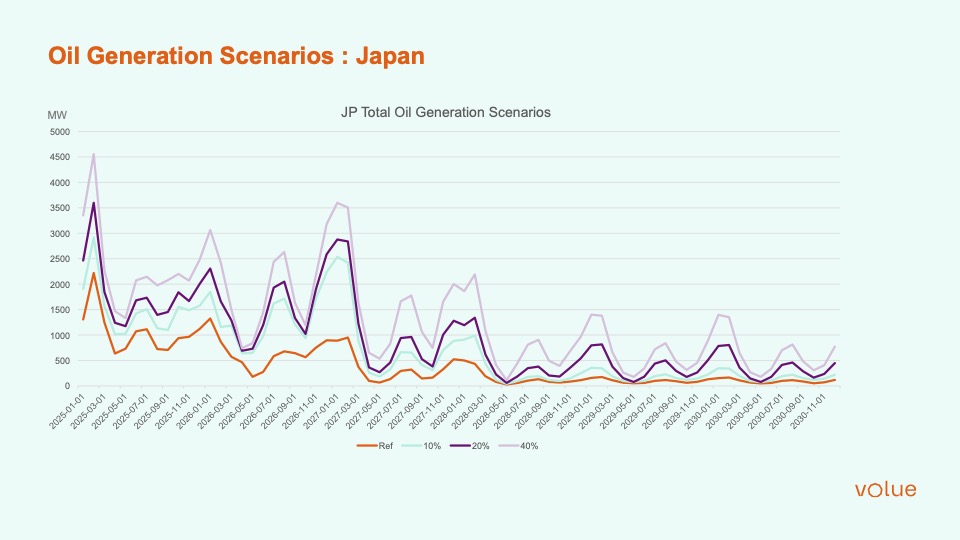

From a generation perspective, higher gas prices reduce the competitiveness of gas-fired output, but the response varies by region due to plant availability, operational constraints and limited interconnection. In regions such as Hokkaido and Tohoku, where coal capacity is more accessible, coal generation increases even under the +10% JKM scenario. Elsewhere, gas continues to operate due to its flexibility role, while oil-fired generation rises in higher-stress scenarios.

Overall, current EEX forward price moves and the JKM sensitivity analysis indicate that even a moderate, sustained rise in LNG prices can materially lift Japanese power prices over the medium term. Price increases of around 2 to 2.5 yen/kWh are already visible in 2026 contracts. If the conflict were to persist and drive both oil-linked LNG costs and spot gas prices higher, impacts would likely be broader, more persistent and closer to the upper-end (+20% to +40%) scenario outcomes, rather than a short-lived spot market shock.

Analysis: Fumi Kumagai, Power Market Analyst